在加利福尼亚州确定合理的受托人费用,往往会面临诸多潜在的利益冲突和法律问题。合理报酬与过高费用的界限常常模糊不清,导致受托人和受益人 alike 都对其权利和义务感到困惑。您究竟有权每年获得信托资产的 1%(或更多),还是应按小时计费获得报酬,这取决于信托文件和加利福尼亚州法律共同确立的若干因素。

在巴尔与杜兹律师事务所,我们的信托管理律师已协助无数受托人和受益人解决了这些棘手的报酬问题,帮助他们在履行受托人职责的同时,确定合理的报酬标准。

受托人费用究竟是什么?

受托人费用是指为管理信托财产而支付给受托人的报酬。这些费用旨在补偿受托人为监督信托资产并根据信托文件及《加州遗嘱认证法》履行职责所投入的时间、精力及专业知识。

担任受托人不仅仅是一个荣誉职位——它伴随着重大的法律义务和潜在的个人责任。受托人负有信托责任,必须完全以受益人的最佳利益为出发点,同时管理往往代表着一个家庭毕生积蓄和遗产的资产。

加利福尼亚州受托人报酬的法律依据

《加利福尼亚州遗嘱认证法》第15681条规定,当信托文件未在条款中明确规定报酬时,受托人有权获得“根据具体情况确定的合理报酬”。“合理”的具体标准被刻意设计得较为灵活,这使得法院能够根据每种情况的独特特点进行评估。

其他相关法规条款包括:

- 第15684条:授权报销与信托相关的合理费用。

- 第15686条:若将补偿金额提高至超过信托文件规定的数额,须提前60天向受益人发出书面通知。

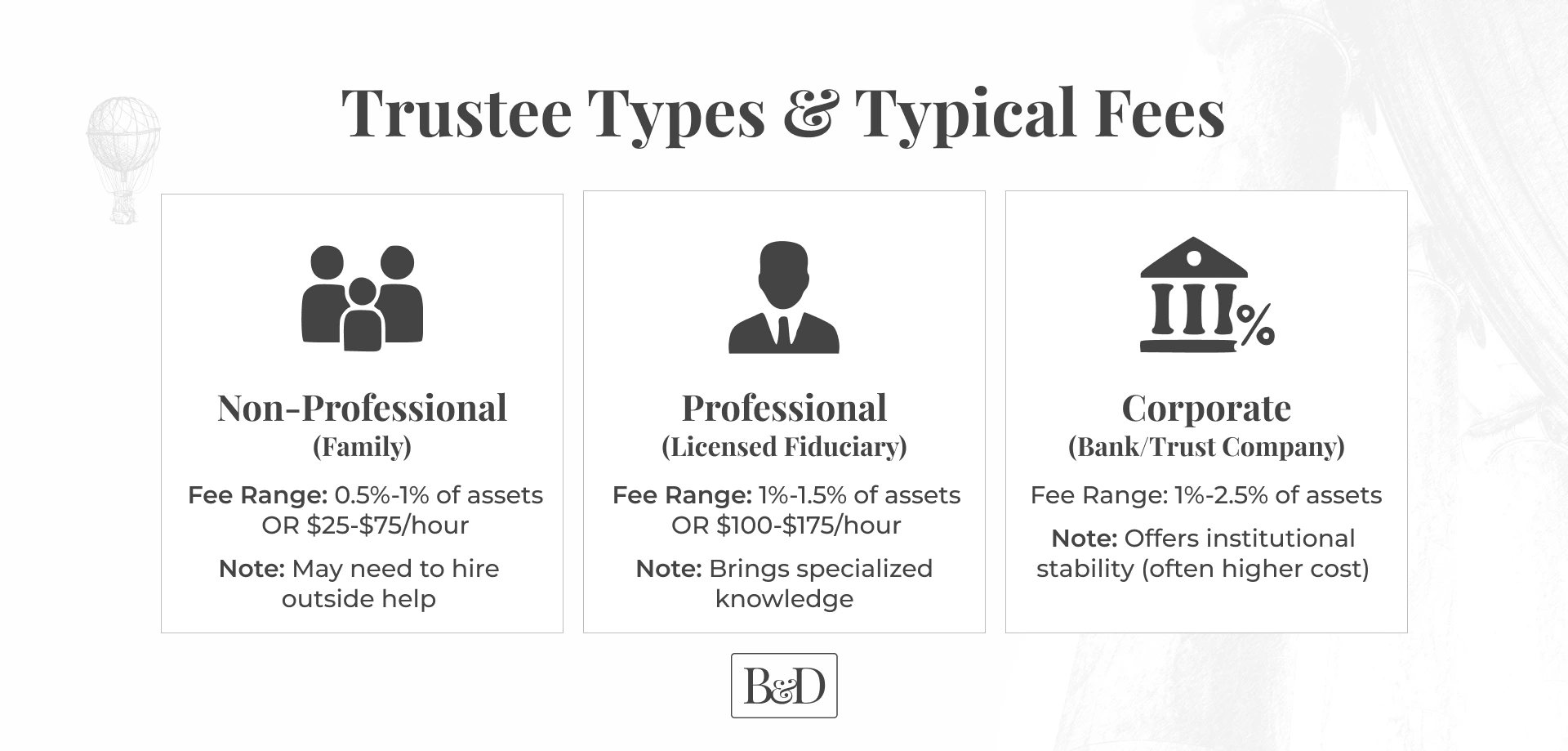

专业受托人与非专业受托人的费用:一项发人深省的对比

受托人的背景和资质对“合理报酬”的界定具有重大影响。加州法院承认,不同类型的受托人在信托管理中具备不同程度的专业知识和效率,这直接影响着适当的收费结构。

让我们来看看不同类别的受托人薪酬通常存在哪些差异(以下仅为示例,未必反映受托人的实际或预期薪酬):

非专业受托人(通常为家庭成员)

- 按百分比计算:每年信托资产的0.5%至1%。

- 时薪:每小时25至75美元。

- 关键考虑因素:通常缺乏专业知识,必须聘请专业人士协助处理复杂事务。

专业受托人(持牌受托人)

- 按百分比计算:每年为信托资产的1%至1.5%。

- 时薪:每小时100至175美元,或更高。

- 关键考量:既要具备专业知识,又要能够收取更高的费用。

公司受托人(银行/信托公司)

- 按百分比计算:每年信托资产的1%至2%(有时更高)。

- 关键考量:提供制度稳定性,但通常收取较高费率。

法院在评估受托人费用时考虑的8个关键因素

当受益人对受托人费用提出异议,或受托人寻求法院批准其报酬时,加州法院不会简单地套用一种通用的计算公式。相反,法官会系统地评估多个因素,以确定在每种具体情况下何为合理的报酬。

以下八个因素构成了加利福尼亚州大多数关于受托人费用的司法裁决的基础:

- 信托资产规模与复杂程度:规模更大、结构更复杂的信托,其报酬相应更高。

- 时间投入:用于信托管理职责的工作时间。

- 管理成效:受托人管理信托资产的成效如何。

- 专业专长:受托人履职时所具备的特殊技能。

- 承担的风险与责任:个人法律责任风险及决策负担。

- 受托人的忠诚度:受托人是否始终如一地致力于为受益人服务。

- 当地标准:信托管理所在县的惯常费用。

- 特殊服务:受托人是否履行了超出常规管理范围的职责。

那些足以证明更高薪酬合理的特殊贡献

基于标准百分比计算的受托人费用通常涵盖常规的信托管理活动,例如资产清点、支付账单、提交常规纳税申报表以及进行分配。然而,加利福尼亚州法律承认,某些信托情况需要超出这些基本职责范围的额外工作。

以下情况通常被视为特殊服务,因此可能有理由在标准费率之外额外支付受托人报酬:

- 企业管理:经营或出售信托持有的企业。

- 复杂的财产事务:管理房地产,尤其是商业地产或异地房产。

- 诉讼辩护:在法律程序中代表该信托。

- 税务复杂性:处理超出常规申报范围的复杂税务情况。

- 受益人关系中的挑战:处理受益人之间的高冲突局面。

实际财务影响:税费与受托人费用

B&D并非税务专业人士;如需税务建议,请咨询您的税务顾问。

受托人报酬不仅关乎确定一个公平的标准,还可能带来重大的税务影响:

- 受托人费用可能构成受托人的应税收入。

- 该信托可将受托人费用作为管理费用予以扣除。

- 对于既是受托人又是受益人的继任受托人而言,收取报酬意味着可能需要就这笔本可通过继承免税获得的款项缴纳税款。

合理安排费用支付的时间,可以最大限度地降低税务影响。与一次性支付大额款项相比,采取小额定期支付的方式,可以避免使受托人进入更高的税率区间。

受托人的基本文件管理规范

为了证明收费的合理性并避免纠纷,细致的记录保存至关重要:

- 聘请税务专业人士。

- 应保留详细的时间记录,以记录所有信托管理活动。

- 创建一个专用的信托管理账户,并为其分配独立的纳税人识别号。

- 请单独记录所有与信托相关的费用,避免将信托费用与个人费用混为一谈。

- 请以特别详尽的方式记录这些非凡的服务。

- 请保留所有收据及信托支出的凭证。

法院在何种情况下可拒绝支付受托人报酬

在以下情况下,法院可以减少或完全不予支付受托人费用:

- 违反受托责任

- 涉及信托资产的自我交易

- 信托管理不善

- 未妥善保存记录

- 将个人资金与信托资金混用

一位湾区受托人动用信托资金购买了一辆全配置皮卡,声称这笔钱是作为其报酬。法院裁定其须全额偿还并支付罚金。

实际案例:受托人费用如何影响分配

案例:一笔价值100万美元的信托财产由一名专业受托人管理,该受托人就三年的管理服务收取了1.5%的年费。

- 受托人费用总额:45,000美元。

- 其他专业服务费(会计师、律师):15,000美元。

- 行政费用总额:60,000美元。

- 受益人可获得的剩余信托资产:940,000美元。

如果由一位家庭成员担任受托人,年费为0.5%,那么总管理费用可能约为30,000美元,从而为受益人额外节省30,000美元。

借助法律指导,维护您的权益

要确定合理的受托人费用,必须仔细权衡诸多因素,包括遗产价值、管理复杂程度、所需时间以及信托文件中规定的具体受托人职责。

在巴尔与杜兹律师事务所(Barr & Douds Attorneys),我们的信托管理律师就以下方面提供精准指导:确定合理的受托人报酬、记录管理活动以证明费用合理性、解决受托人薪酬纠纷、建立规范的信托会计体系,以及在受托人面临不合理的费用质疑时为其进行辩护。我们的团队随时准备通过量身定制的解决方案,在符合法律要求和受托责任的前提下,全力维护您的权益。 立即致电(925) 660-7544,获取关于加州受托人费用的免费咨询,或在线预约!